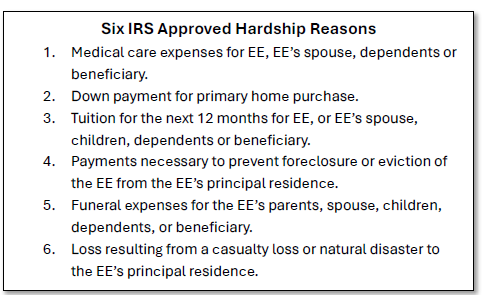

IRS Approved Hardship Checklist

Please refer to this document as a guiding tool when working with a participant that's submitting proof of hardship.

IRS Approved Hardship Checklist OneNote

General Information

Medical expenses

Medical care expenses for the employee, the employee’s spouse, dependents or beneficiary.

Acceptable proof: Patient name is the ptp, even if the bill is in someone else's name. Travel and lodging is also considered part of the hardship, this is the only case a credit card bill can be used for a hardship. Travel/lodging would be up to $50 per person (only patient and their parents in the case of a minor) per day, meals are not included. Travel/lodging can only be submitted after the stay.

Unacceptable proof: Plastic/cosmetic surgery

Medical expenses bills submitted should be as recent as possible. The date of the bills should be a "paid as of" date. Our preference is within 60 days, but during review Rebecca will confirm if the bills are acceptable or not.

For example, if the proof says the hospital visit was in January of 2024 and the balance is still outstanding. We need something that says "This amount is outstanding as of February 2024" or something along those lines.

Bills cannot be in collections.

Medical Expenses Covered Under IRS Section 213 for Hardship.pdf

Future tuition for college

Laptop and books can be considered related education fees, meaning they are acceptable as proof. If this is the request without the tuition bill, we will need proof of the request is for a current student. Proof could be an admissions document or a paid tuition bill.

Next, we need reasonable estimates for the laptop and books including screenshots of information online. Once these expenses are on a credit card, they are no longer considered a heavy or unforeseen expense and would not be eligible for a hardship withdrawal.

Down payment for home purchase

Costs directly related to the purchase of an employee’s principal residence.

Unacceptable proof: Mortgage payments, Sales agreement/Real Estate agreement to purchase property.

Additional Information about Purchase of Primary Residence

Must provide a copy of the contractual agreement to build or purchase primary residence, and documentation to verify the funds due at closing.

- A copy of the Final Closing Document that includes ALL of the following:

- The Purchase Price

- The Closing date/completion date – this must be in the future

- The Street address of the property being purchased / built

- Dated Signatures of BOTH the buyer and seller

If building the home and the land is already owned:

- A copy of the notarized deed to the land in the participant’s name

- A copy of the signed construction contract that includes items on the above list

- Other reasonable proof such as building permits or receipts

If this is a private sales contract, a non-standardized purchase agreement, a for sale by owner contract, manufactured home contract or any other type of hand-written contract between buyer and seller it must be signed, dated and both signatures notarized. This includes any purchase agreement that does not include a real estate agents name and/or company name.

2. Documentation to show the funds due at closing. This must be the final disclosure form, not an estimate/agreement. Must include the following:

- Participant’s Name

- The Purchase Price

- The Closing date/completion date – this must be in the future

- The Street address of the property being purchased / built

- Funds due at closing, cash from borrower due at closing, or cash due at closing. Cannot be an estimate.

If not available, a letter from the mortgage company or realtor on letterhead referencing the participant’s name, property address, closing date, and funds due at closing. This must be signed, titled and dated by a representative of the mortgage company.

Prevention from foreclosure or eviction

Prevention from foreclosure or eviction from the participants primary residence requires documentation showing the following:

- Is this the participants principal residence? CSR should ask on the call.

- Address of the residence.

- Type of event (foreclosure or eviction).

- Name and address of the party that issued the foreclosure or eviction notice.

- Date of the notice of foreclosure or eviction.

- Due date of the payment to avoid foreclosure or eviction.

If we receive proof and it does not meet these requirements, we will deny the request.

The hardship must be used to prevent eviction. If we receive documentation with an expired date to pay, the payment won't keep the participant from losing their home.

If the participant's name is not on mortgage, but the spouse's name is, we need more information before we can make a determination. We need to see the foreclosure notice to ensure a few things:

1) That it truly is a foreclosure notice and would qualify.

2) We need her husband's name to see if we possibly have him listed as a beneficiary on her plan.

3) The notice would also give us the address so we can ensure it lines up with the address we have on record.

If they will send in the notice, we can determine if it qualifies for a hardship.

Property damage

- Must be the homeowner.

- Due to a casualty loss: limited to principal residence repairs.

- Due to a natural disaster

- The disaster hardship can cover other expenses and losses, including lost income. For example, if TTC was flooded and no one can work and employees lose income.

- Proof would be contractor/supply store estimates for the repair of the residence

- Proof for loss of income, we will verify by the transaction specialist emailing the employer for confirmation

Funeral Expenses

- Participant must be the responsible party, and the bill must be made out to them.

Understanding our role here at TTC

For hardships, the Plan Sponsor should review any hardship request they receive from Lynda before approving. The review includes checking their files for past requests they’re signing off on. If they see anything questionable, let us know and we will request additional documentation. The Plan Sponsor needs to know that they need to take some accountability with signing off on hardship distributions. We review the paperwork presented to us to determine if it is an eligible hardship, but we are not combing through the files to see if the expenses have ever been requested before.

If the IRS ever audits or questions the participant, the blame completely falls on the participant, and not the plan sponsor and not us. Plan Sponsors should be diligent to review what is requested to approve. Our stance is that the Plan Sponsor knows their employees better than we do and if they think something is fishy, we are happy to deny the withdrawal or ask for more proof.